- Investors continue to add funds to MUNI bond funds; last week, 260MM was added from retail investors. The prior week saw a 262MM inflow, indicating that retail investors have been seeking tax-exempt paper over the past few months. The overall calendar continues to decline as we move into the balance of this year, sitting around 7.2B compared to around 14B on the average.

- Bloomberg reported yesterday, 12/17, that they expect inflation to resume its downward trajectory in the next few months, while job prints will likely remain weak. Over time, that combination should weaken the FOMC’s hawks’ resistance to rate cuts. Bloomberg data is also calling for a 100bps cut in 2026, more than the market is currently anticipating.

- Underlying US inflation rose (reported today, 12/18) in November from a year earlier at the slowest pace since early 2021, according to a report complicated by the federal government shutdown. The core consumer price index, which excludes the often-volatile food and energy categories, increased 2.6% in November, compared with 3% annual advance two months earlier. The overall CPI rose 2.780% year over year in November. This report indicates inflation pressures are easing after remaining stuck in a narrow range since earlier this year.

- With the CPI numbers released today, 12/18, it is unclear whether the report will sway policymakers who remain divided on the course of rate cuts next year. We see a 50bps cut at a minimum for 2026, and CPI numbers continue to show signs of decreasing over the next 12 months.

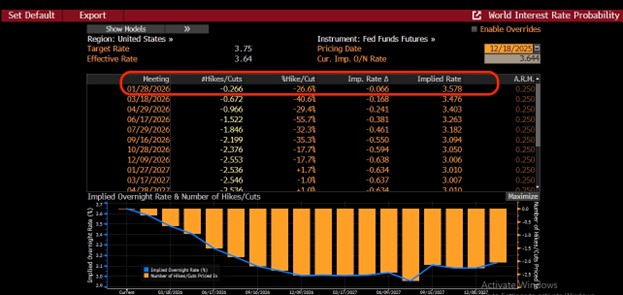

- Currently, the percentage of a rate cut for January is sitting at 26.50% (graph attached). Yields on the 10T have broken the 4.20% resistance level this morning with the CPI numbers, sitting at 4.11% as we publish this. Across the curve this morning, yields are down, with the longer end of the curve moving down more compared to the shorter end of the curve.

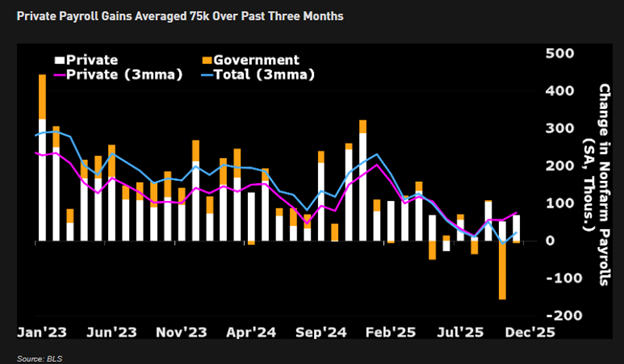

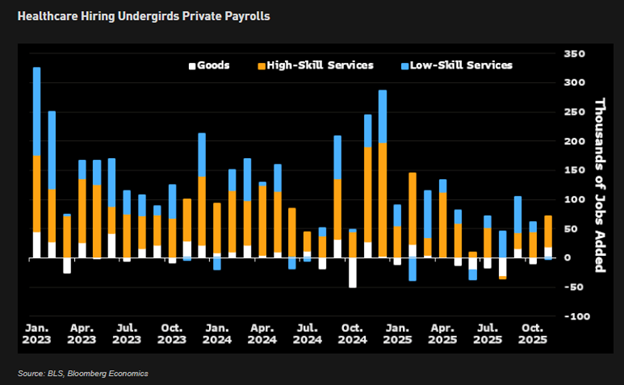

- As we saw, the double jobs report vindicated the FED’s decision to cut rates in December. Hiring was concentrated in education and health care, as well as AI-related construction, but not much else. The jobless rate rose briskly, and it’s possible the Sahm Rule for identifying a recession would have been triggered if October’s household survey had been conducted. I have attached a graph showing private payroll gains, which averaged around 75K over the past three months.

- MUNI credit spreads remain resilient headed into 2026, and most states and issuers remain well bid for. We have seen an uptick in buyers for paper over the last few weeks (shown by the inflow of capital in MUNNI funds), which has created a flurry of activity in our markets, driven by tax trades and strong credits in general.

Bottom Line

Yields are steady so far this month, issuance continues to decrease, and with the 25bps cut last week, we have not seen much action in the markets. However, with this said, the FED will remain vigilant and hold their cards “close to their vest” as they make comments at the next meeting in January 2026. If you are a long-term buyer, the longer end of the curve should perform well. Pay attention to your call dates, as you will want some call protection as we move through 2026.

Rate cut percentage chart

Private Payroll Gains Over Three Months

Healthcare Jobs Added

Securities offered through NewEdge Securities, LLC, member FINRA and SIPC. The DRL Group is not a subsidiary or control affiliate of NewEdge Securities, LLC. NewEdge Securities, LLC. has no affiliation to BondDesk Trading LLC or BondTrader Pro, or Tradeweb Direct, Bondpoint, TMC, Market Axess or any ECN.

Yield to call (YTC) is not indicative of total return; this yield is valid only if the security is called. Bonds may or may not be called, or be callable on multiple dates or, in other cases, called any date following the first call date, so yield to call is based on the earliest stated call date. Discounted bonds may be subject to capital gains tax. Bonds may be subject to OID (Original Issue Discount). Prices and availability may change at anytime without notice.

Do not buy bonds based on the Yield to Call (YTC). Insured bonds are issued for timely payment of principal and interest only. Insured bonds do not cover potential market loss and are subject to the claims paying ability of the insurance company.

Non-rated (NR), With-Drawn (WR), or below investment grade bonds, lower rated bonds, carry a greater potential risk of default & should be considered by sophisticated investors only.

This document is for informational purposes only and does not replace or serve as a substitute for your official monthly statement generated by NFS. Please refer to your official statement for accurate and comprehensive account details.

Bonds may be subject to capital gains tax. This summary is for informational purposes only and is not an offer or solicitation for the purchase or sale of any security or a recommendation or endorsement of any security or issuer. NewEdge Securities, LLC. and DRL Group make no representation about the accuracy, completeness, or timeliness of this information. Bonds could also be subject to the DeMinimis Rule, please consult with your tax advisor for further clarification.

Call us at 281-398-8600 to invest in these or any of our other offerings today.