The Fed is changing hands and hike talk is back. Here is what it means for your bonds.

The Signal

Tuesday morning, 10-year Treasury yields fell 10 basis points to 4.57% in a single session. Thirty-year yields dropped to 5.11%. The catalyst was a White House pool report suggesting the U.S. and Iran were in the “final stages” of a deal that could ease energy prices and the inflation concerns tied to them. By the afternoon, the market had given back a portion of those gains as traders waited for confirmation.

This is the market we have been describing to clients for weeks: on again, off again. A single headline can move yields 10 basis points in either direction. The $31 trillion Treasury market is trading on geopolitical news flow, not fundamentals — and that creates both risk and opportunity for disciplined investors.

The inflation backdrop driving that volatility has not softened. April’s CPI came in at 3.8% year-over-year — the fastest pace since 2023 — and the producer price index rose 6% over the same period, with core PPI up 5.2%, the largest advance in more than three years. Both readings are war-driven: energy costs from the Iran conflict flowing into transportation and downstream prices. The Fed’s internal consensus is fracturing in response. Futures markets are now pricing in a full rate hike by mid-2027 — a scenario that was unthinkable at the start of the year.

The market is telling you something this week. The question is whether you are positioned to hear it — and act on it.

What’s Driving It

Warsh takes the chair — tone shift ahead

Kevin Warsh will be sworn in Friday, succeeding Jerome Powell, who has been serving in a temporary capacity since his official term ended last week. We do not expect Warsh to cut rates out of the gate — the inflation data makes that politically and economically untenable. What we do expect is a modest shift in tone: somewhat more hawkish in posture than Powell’s final meetings, but not aggressively so. The FOMC minutes released this week underscore why: “many” officials discussed dropping the easing bias entirely and flagged that “some policy firming would likely become appropriate” if inflation remained persistently above 2%. That language is not a bluff.

The hike conversation is real

Two months ago, the street consensus was cuts in 2026. Today the conversation has shifted to no cuts in 2026, with possibly one or two in 2027. Fed officials — including Philadelphia Fed President Anna Paulson this week — are conditioning any easing on “sustained progress” against inflation that the data is not yet showing. NY Fed President John Williams has pushed back on the need to hike, but the FOMC minutes make clear that his view is not the committee’s center of gravity right now. We would not recommend betting on zero cuts — things can change quickly, and we’ve seen as much in the last three weeks — but the probability of cuts in 2026 has narrowed considerably.

Record supply is reshaping the market

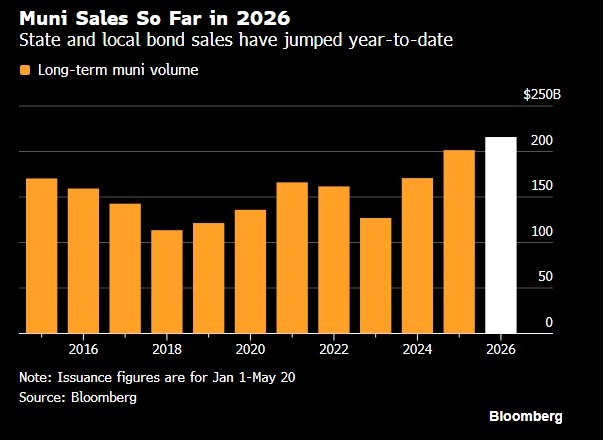

Municipalities have sold approximately $216 billion in debt so far this year through May 20 — up roughly 10% from the same period in 2025 and on pace to challenge or exceed last year’s record $570 billion. Billion-dollar deals have become, in the words of one senior underwriter at the Bond Buyer’s conference this week, “much more of the norm.” California sold $2.4 billion in March. Two New York deals exceeded $2 billion this year. Atlanta’s airport is expected to bring another $1 billion to market in August as part of a $10 billion capital modernization program. The average deal size has nearly doubled since 2016. The chart below tells the story clearly.

Source: Bloomberg. Issuance figures are for Jan 1–May 20.

The volume creates a paradox. More supply means more selection opportunity — but it also means more competition for investor dollars, which can weigh on prices if demand fails to keep pace. Hitting $600 billion for the year would require averaging roughly $50 billion a month for the remainder of 2026. That is achievable but not certain, and the path there runs directly through the Fed’s posture under Warsh and the outcome of November’s midterms. We are watching both.

Muni yields: 40 bps above February and building

April’s muni rebound was the largest in 11 years, clawing back part of March’s rate shock. But yields still sit roughly 40 basis points above February levels, keeping the entry case intact. This week, longer-dated Chicago Water and Sewer paper touched a 5% yield-to-worst — a concrete illustration of where the market is pricing quality paper right now. Meanwhile, muni yields moved an additional 5 to 7 basis points higher across the curve this week in response to the inflation prints, widening the entry point modestly further.

Electronic trading hits record share — DRL is ahead of it

A Barclays report released this week found that electronic trading in munis totaled 19% of total volume in February, nearly double the 10% recorded in 2023. The municipal bond market is

becoming faster and more liquid — a structural shift that rewards dealers with the systems to navigate it. DRL has been active in this space for over a decade. Our platforms are designed to find securities that meet your objectives and execute at levels that reflect that broader market visibility, not a single dealer’s inventory.

Technicals are setting up constructively

Dealer inventories are building ahead of pre-summer activity. Relative value remains supportive — munis maintain a tax-equivalent yield advantage over comparably rated corporates. Fund inflows and seasonal reinvestment demand are beginning to stir and should help absorb supply in the weeks ahead. We expect this dynamic to keep some upward pressure on yields near-term, which is precisely what creates the buying window.

Our Take

We covered much of this in detail on our May 19th webinar — and the week’s events have moved largely in line with what we laid out there. If you missed it, the replay is available for one week only. We’d encourage you to watch it.

Our posture has not changed: we are slow buyers at these levels. The combination of yields 40 basis points above February, a constructive technical setup, and the beginning of seasonal reinvestment demand makes this a favorable environment to be adding quality paper — selectively and patiently.

The key word is selectively. This is not a moment to chase the market. Record supply is building — $216 billion already issued this year, with more mega-deals in the pipeline — and while volume creates opportunity, it also creates absorption risk if demand softens. Treasuries are running the show on a day-to-day basis, and the tone could shift again quickly if the Iran situation evolves or if summer technicals fade. The right posture is to nibble the dip, not chase it.

What the volatility is creating, though, is something genuinely useful: real peaks and valleys on both the buy and the sell side. A 10-basis-point move in a single session is not noise — it is opportunity, if you are positioned to act on it. That is exactly what our team is watching for on your behalf.

A note on risk: the variables we are monitoring closely are the trajectory of the Iran conflict and its effect on energy prices, the pace of disinflation heading into Warsh’s first FOMC meetings, and the volume and absorption of new muni supply over the coming weeks. None of these represents a worst-case scenario in our base case — but all are live, and all could move quickly.

Recommendations

Be a slow, selective buyer — but be a buyer

With yields 40 basis points above February and quality paper like Chicago Water and Sewer touching 5% YTW, the income case for munis is real. We are not suggesting deploying everything at once. We are suggesting that sitting entirely on the sidelines in this environment means giving up yield that may not be available when the picture clarifies. And with record supply hitting the market, the selection opportunity is unusually broad right now — which is precisely where having a specialist who can see across the full market, not just a single dealer’s inventory, makes a material difference. Add quality paper in measured increments.

Use the volatility — on both sides

The on-again, off-again dynamic we have been describing creates actionable moments. A 10-basis-point rally on an Iran headline is a selling opportunity for clients who are overweight duration. A 10-basis-point selloff on a hot inflation print is a buying opportunity for clients who have been waiting for a better entry. Know which side of that trade you are on, and be ready to move. Our team is watching these moves in real time.

High-tax-state clients: the after-tax case has strengthened

The yield widening of the past several weeks has improved the after-tax math for clients in California, New York, New Jersey, and similar high-tax states. Double-exempt paper is offering taxable-equivalent yields that compare favorably to anything in the investment-grade fixed income universe right now. If you have not reviewed your in-state muni allocation recently, this is a good week to do it.

New York clients: monitor the city budget

Mayor Mamdani’s decision to pull the proposed property tax increase from the executive budget is a near-term positive for NYC real estate-backed credits. The underlying deficit, however, has not been resolved — watch for what replaces it in the final budget. We will keep New York clients updated as the picture develops.

Stay up in credit quality

High-yield munis have not widened meaningfully despite the broader rate volatility. Investors are not being adequately compensated for credit risk at current spreads. We continue to favor AA and AAA rated general obligation and essential-service revenue bonds. Quality discipline is the right posture.

If you would like to talk through any of this in the context of your specific holdings, reach out. The market is moving fast right now — and that is exactly when having a team watching it alongside you matters most.

Let’s Talk

If you would like to discuss any of the above in the context of your portfolio, reach out. This market environment rewards preparation — and that is exactly what we are here to help with.